Sequence Risk

The order of returns can matter

Key Takeaways

- Market losses can feel different in early retirement because a household may be taking money out.

- Sequence risk means the order of returns can matter, even when long-term averages look similar.

- Withdrawals during early market declines can create pressure on a retirement-income plan.

- The concept does not mean markets are bad. It means retirement is different from saving for retirement.

What does this actually mean?

Market losses can feel bad at any age. But market losses can feel different in early retirement.

During working years, a person may still be adding money to accounts. In retirement, a person may be taking money out.

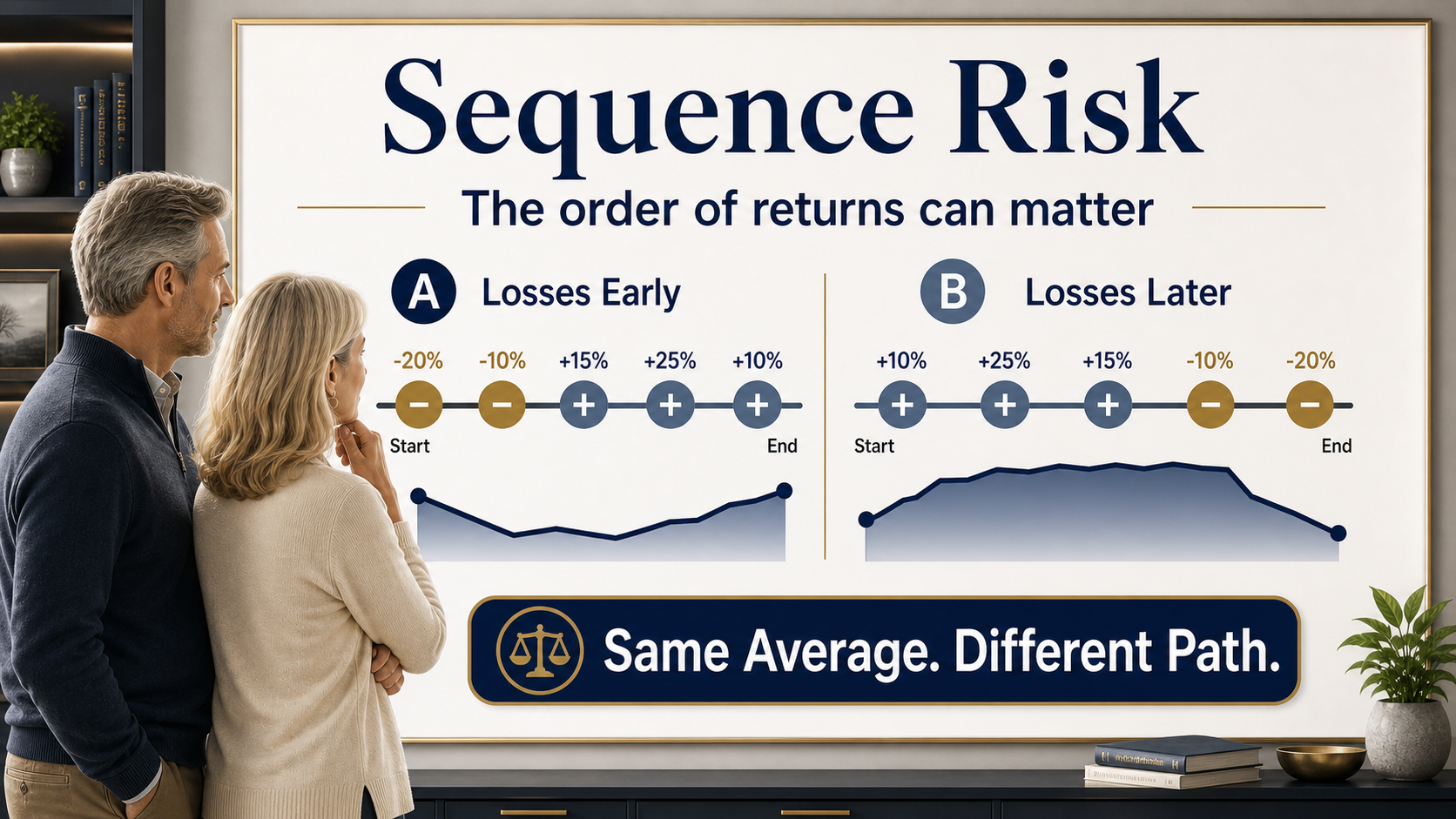

Why order matters

Sequence means order. Sequence risk means the order of market returns can matter.

Two retirees can have the same average return over many years. If bad years arrive early for one of them, the experience can feel very different.

Where does Aftura fit?

RetireIQ helps visitors see why income timing, spending needs, and market exposure belong in the same conversation.

How can the same average return feel different?

Two retirees can earn the same average return over time and still have very different experiences.

If one retiree gets poor returns early while taking withdrawals, the account may feel more pressure than if the poor returns arrive later.

Why do withdrawals change the math?

When a person is saving, market drops can be painful but new contributions may continue. In retirement, withdrawals may continue instead.

That is why early retirement can feel different. The account is being asked to recover while also sending money out.

Why does flexible spending help?

Flexible spending can reduce pressure during difficult market periods. Some expenses may be delayed or adjusted. Other expenses may be harder to change.

Knowing which expenses are flexible can help a household understand how exposed it may feel during bad market years.

The planning takeaway

Sequence risk does not mean markets should be avoided. It means the income plan should understand timing.

A retirement paycheck system may need different buckets for near-term spending, long-term growth, and dependable income.

What mistakes should readers avoid?

The first mistake is treating one visible number as the whole answer. In retirement, the visible number may be an age, a savings balance, a withdrawal rule, a premium, or a tax estimate. The visible number matters, but it is rarely the whole story.

The second mistake is assuming that one household's answer should become another household's answer. Two families can look similar from the outside and still have very different income needs, health costs, tax situations, family goals, and comfort levels.

The third mistake is waiting until the decision feels urgent. Retirement questions are easier to understand when they are reviewed before a deadline.

How should readers think about tradeoffs?

Most retirement decisions involve tradeoffs. More flexibility may mean less certainty. More certainty may involve costs or limits. More income today may affect income later. More protection may reduce access to money in some situations.

This is why the goal is not to find a perfect answer from one article. The goal is to understand the moving parts well enough to have a better next conversation.

A clear tradeoff is not a problem. It is useful information. It helps a household see what it may be giving up and what it may be getting in return.

Why can averages mislead people?

Averages can help people learn, but averages can hide personal details. Average returns, average inflation, average healthcare costs, and average retirement ages may not describe a specific household.

Averages are most useful when they start a question. They become risky when they end the question.

A better approach is to use averages as a doorway, then review the personal facts that could change the result.

How does this connect to RetireIQ?

RetireIQ is designed to organize the questions behind the article. It does not replace a professional review, and it does not tell a visitor what financial product to buy.

Its job is diagnostic. It helps make income pressure, inflation pressure, timing questions, and planning gaps easier to see.

That kind of diagnosis can make a future conversation more useful because the visitor is no longer starting from a blank page.

Selected references

- Aftura education review of sequence-of-returns risk and withdrawal sustainability concepts.