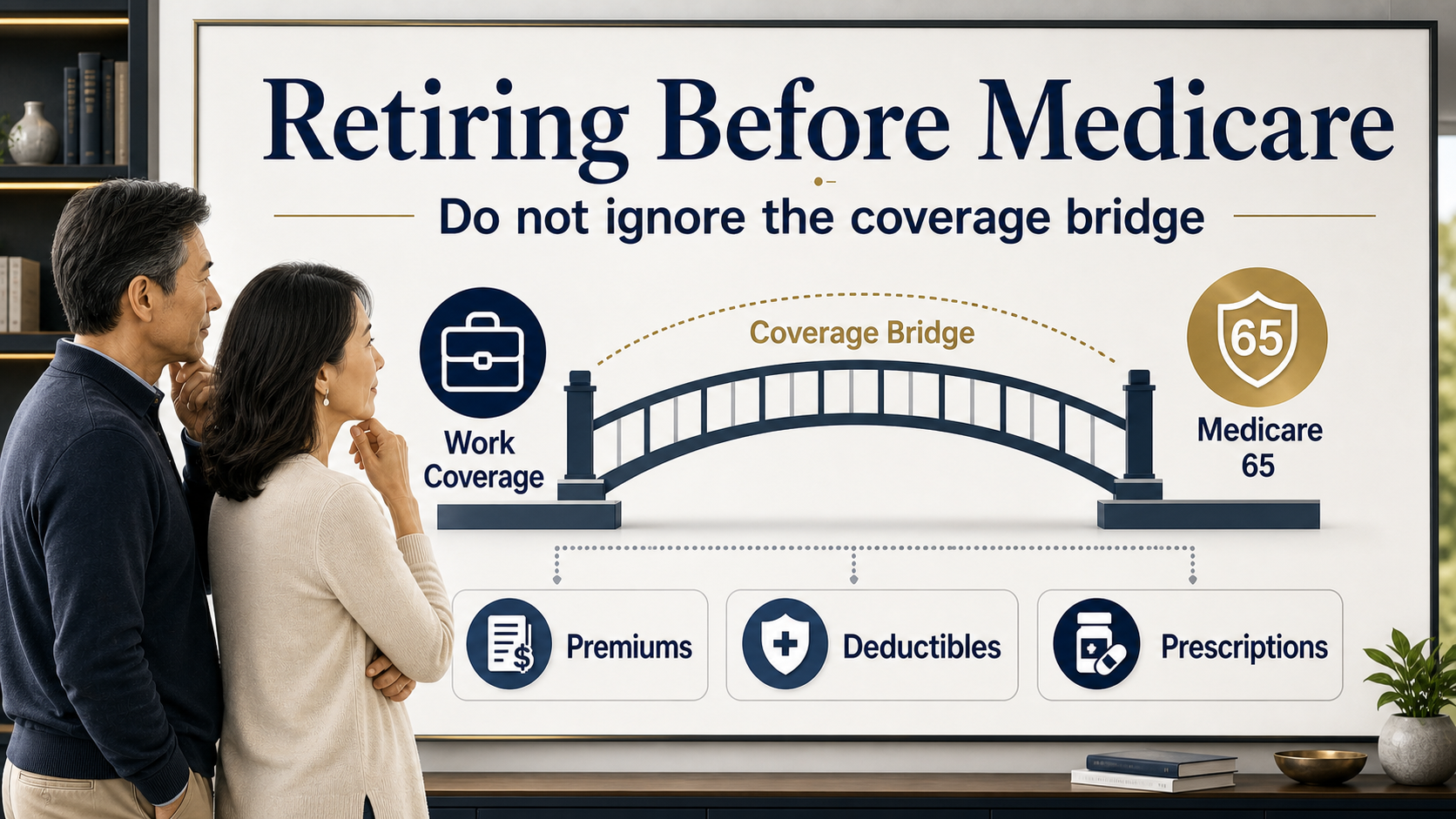

Retiring Before Medicare

Do not ignore the coverage bridge

Key Takeaways

- Many people connect Medicare with age 65, but some people want to stop working earlier.

- The years between work coverage and Medicare can create a coverage bridge.

- Premiums, deductibles, prescriptions, and out-of-pocket costs can change how much income feels usable.

- This is a planning question, not a recommendation for any specific coverage choice.

What does this actually mean?

Many people think retirement is mostly a work decision. Before age 65, it may also be a health coverage decision.

The coverage bridge is the period between leaving work coverage and reaching Medicare eligibility.

Why the bridge matters

The bridge may be short. It may be several years. It may involve a spouse's plan, COBRA, marketplace coverage, retiree benefits, or another option.

Health coverage affects the retirement paycheck. Premiums, deductibles, prescriptions, coinsurance, and out-of-pocket costs can change how much income feels usable.

Where does Aftura fit?

Aftura can help make the coverage question visible before someone treats retirement as only a savings decision. It does not recommend a coverage option.

How can the coverage bridge change the budget?

A retirement budget can look comfortable until health coverage is added. Before Medicare, the cost of coverage can be one of the biggest planning questions.

That cost may last only a few years, but a few expensive years can still matter.

Why can timing change the outcome?

A person who retires at 64 may need a short bridge. A person who retires at 60 may need a longer bridge.

The length of the bridge can affect how much savings must cover before Medicare begins.

The planning takeaway

Retiring before Medicare is not only a work decision. It is also a health coverage decision.

The goal is to see the bridge before stepping onto it.

What mistakes should readers avoid?

The first mistake is treating one visible number as the whole answer. In retirement, the visible number may be an age, a savings balance, a withdrawal rule, a premium, or a tax estimate. The visible number matters, but it is rarely the whole story.

The second mistake is assuming that one household's answer should become another household's answer. Two families can look similar from the outside and still have very different income needs, health costs, tax situations, family goals, and comfort levels.

The third mistake is waiting until the decision feels urgent. Retirement questions are easier to understand when they are reviewed before a deadline.

How should readers think about tradeoffs?

Most retirement decisions involve tradeoffs. More flexibility may mean less certainty. More certainty may involve costs or limits. More income today may affect income later. More protection may reduce access to money in some situations.

This is why the goal is not to find a perfect answer from one article. The goal is to understand the moving parts well enough to have a better next conversation.

A clear tradeoff is not a problem. It is useful information. It helps a household see what it may be giving up and what it may be getting in return.

Why can averages mislead people?

Averages can help people learn, but averages can hide personal details. Average returns, average inflation, average healthcare costs, and average retirement ages may not describe a specific household.

Averages are most useful when they start a question. They become risky when they end the question.

A better approach is to use averages as a doorway, then review the personal facts that could change the result.

How does this connect to RetireIQ?

RetireIQ is designed to organize the questions behind the article. It does not replace a professional review, and it does not tell a visitor what financial product to buy.

Its job is diagnostic. It helps make income pressure, inflation pressure, timing questions, and planning gaps easier to see.

That kind of diagnosis can make a future conversation more useful because the visitor is no longer starting from a blank page.

Selected references

- Medicare.gov: Medicare eligibility and coverage basics.

- Healthcare.gov: marketplace coverage education.